What Your Business Bank Is Costing You in Yield, Fees, and Engineering Hours

Most founders already suspect their business bank is underperforming. What they rarely have is a number. This guide quantifies four specific cost categories (yield gap, fee structures, FX markups, and engineering overhead) and gives you a calculation method for each. By the time you finish, you’ll know whether banking inertia is costing your company hundreds, thousands, or five figures annually, and exactly what to do about it.

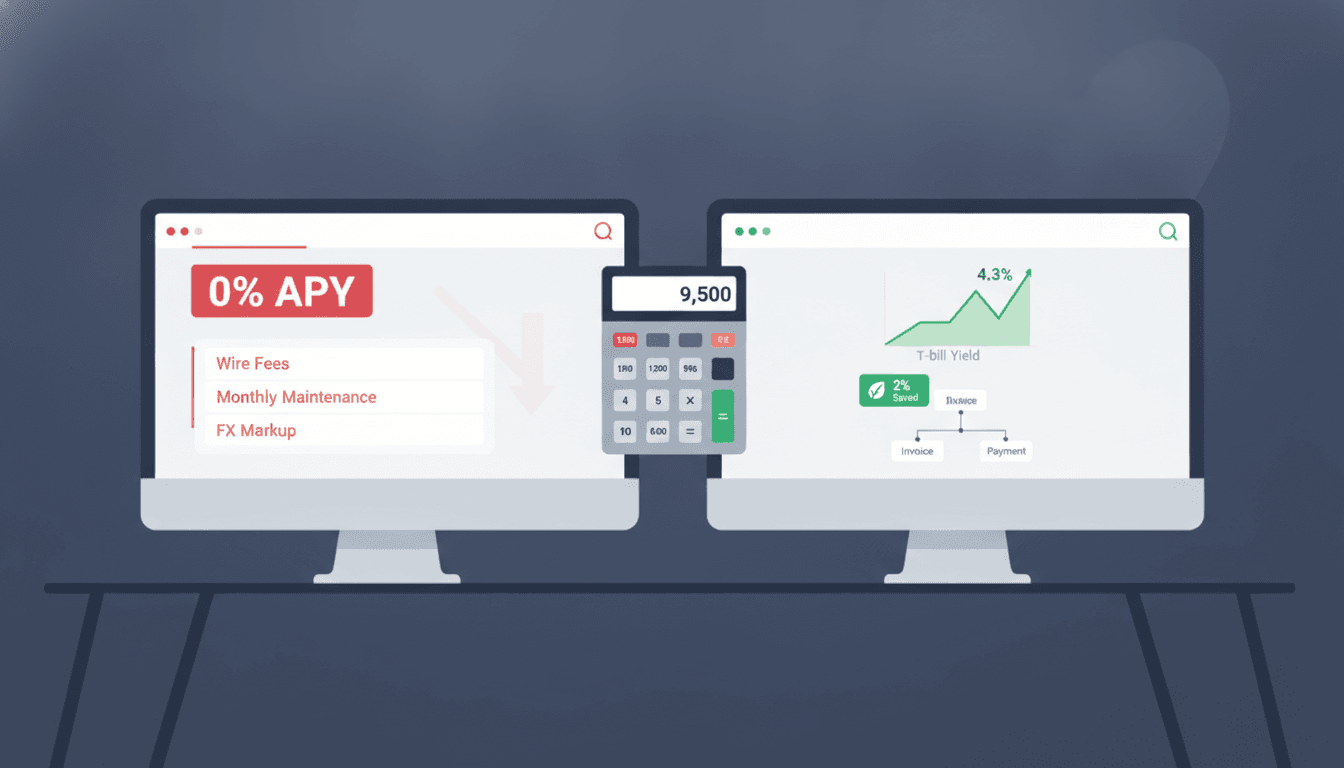

Your operating account is probably earning close to nothing. The average business checking account pays under 0.1% APY, while money market funds and short-duration Treasuries are currently yielding north of 4%. If you’re holding $2M in operating cash, that delta costs you roughly $80,000 a year in forgone yield, and that is before you account for wire fees, ACH fees, and the engineering time your team burns maintaining bank integrations.

Most finance teams treat this as background noise. It compounds quietly across every idle cash balance, every manual reconciliation, and every API outage that delays a vendor payment.

The Yield Delta Your Bank Isn’t Advertising

Traditional banks profit from the spread between what they pay depositors and what they earn deploying that capital. Keeping your yield low is the business model.

And, banks are not incentivized to notify you that better-yielding alternatives exist. The business model depends on depositor inertia. T-bills can be purchased directly through a brokerage, sold on the secondary market same-day, and auto-rolled at maturity without requiring active management.

The fix requires moving excess operating cash into instruments that actually pay market rates, such as Treasury bills, money market funds, or short-duration bond ETFs, and keeping only the float you need for near-term payables in checking. The operational friction of doing this manually is real, but it’s a one-time setup cost, and the annual yield pickup typically covers a mid-level engineer’s salary.

Fee Structures That Scale Against You

Business banking fees are designed to be opaque. Wire transfers typically cost $15–$35 per domestic transaction and $35–$50 international. ACH fees run $0.20-$0.50 per transaction. Account maintenance fees add $15–$50 per month. None of these are large individually, but a company running 500 vendor payments a month is paying $1,000–$2,500 in transaction fees alone, every month, for the privilege of moving its own money.

Fintechs and newer banking-as-a-service platforms have largely eliminated per-transaction fees. Mercury, Relay, and Brex all offer free ACH and reduced-cost wires. The trade-off is counterparty risk and FDIC coverage structure. Most of these platforms hold your funds at partner banks, so you need to verify coverage limits before consolidating balances above $250,000.

How to audit your current fee exposure

Pull 90 days of bank statements and flag every line item: monthly maintenance, wire fees, ACH fees, service charges. Sum them and multiply by four to annualize. This is your fee baseline; the costs that actually appear on paper. Most finance teams who run this exercise are surprised by the total before they’ve touched yield, FX, or engineering overhead.

Engineering Hours Are the Hidden Cost

Every bank integration your engineering team maintains is a liability. Core banking APIs have uptime SLAs that allow for hours of downtime per month. For instance, Plaid’s published uptime data shows many instances of degraded performance across multiple institution connections. When your bank’s API goes down, your cash flow data goes stale, your reconciliation breaks, and someone on your team has to investigate.

The engineering cost compounds in two ways. Your team writes and maintains the integration code. When the bank changes its API (which often happens with almost no notice, btw), your team rewrites it. A single bank integration typically consumes 2–4 weeks of initial engineering time and 1–2 weeks per year of maintenance. Multiply that across multiple banking relationships and you’re looking at a meaningful fraction of an engineer’s annual capacity.

The practical answer is to minimize direct bank API integrations where possible by routing through a banking aggregator or a treasury management platform that abstracts the underlying bank connections. You trade some control for reliability, and the reliability is usually worth it.

Quantifying the integration liability

Time one complete AP/AR cycle from invoice receipt through payment and reconciliation. Multiply by your annual number of pay cycles, then multiply by your blended hourly cost. This is your labor exposure: the number that compounds every time you add a vendor or hire someone to manage the backlog. At $120 per hour blended cost and 10 hours per week, the annual exposure is $62,400 before a single line of integration code is written.

What Good Treasury Infrastructure Looks Like

A well-structured treasury setup for a growth-stage company separates cash into three tiers: operating cash (30–60 days of runway in checking), short-term reserves (3–6 months in money market or T-bills), and longer-duration holdings if the business carries material cash beyond operating needs.

The operating account should be at a bank with strong API reliability and minimal per-transaction fees. The reserve account should be at a custodian or brokerage that lets you hold Treasuries or money market funds directly. Fidelity, Schwab, or Interactive Brokers all support this for business accounts. Moving money between the two tiers on a predictable schedule keeps operational complexity manageable without leaving excess cash idle in a low-yield checking account.

The engineering integration for this pattern is simpler than it sounds. You need one reliable connection to your operating bank for daily cash position data, and one to your custodian for reserve balance and yield reporting. Both feed into your financial model. The total integration surface is smaller than most teams assume, and the yield improvement pays for the setup in weeks.

The Inertia Tax

Most founders already know their bank is underperforming. They just don’t act on it. The math behind that inertia is damaging. A 2025 Wise-commissioned report found small businesses collectively paid $153 billion in hidden or undisclosed bank fees in the prior year. Averaged across individual entrepreneurs, that would be around $4,400 per year in fees. For those with international operations, the number climbs to $7,200.

These fees don’t show up on a statement labeled “cost of staying.” They’re embedded in spreads, absorbed into wire charges, and baked into exchange rates, making them invisible by design.

At $4,400 per year, three years of switching inertia costs a typical founder more than $13,000. At $7,200 for internationally active businesses, that number exceeds $21,000 over the same window. Neither figure accounts for yield gap on idle balances, which compounds separately on top of the fee exposure.

Idle Cash: The Yield Gap Your Checking Account Is Running

Your startup’s checking account is probably earning somewhere between 0% and 0.5% APY. Meanwhile, 4-week and 13-week Treasury bills are yielding around 4.3%. That delta compounds against every dollar sitting idle.

The formula: Annual Yield Gap = (T-bill rate − current checking APY) × average idle balance.

| Idle Cash Balance | Checking APY | T-bill Rate | Annual Yield Gap |

|---|---|---|---|

$250,000 | 0% | 4.3% | $10,750 |

$500,000 | 0% | 4.3% | $21,500 |

$1,000,000 | 0% | 4.3% | $43,000 |

The most common objection to putting idle cash into Treasuries is liquidity—the fear of locking up funds you might need quickly. T-bills can be sold on the secondary market same-day without waiting for maturity and without incurring trading fees, so the liquidity tradeoff founders assume is largely imaginary.

Your average idle balance is easy to calculate: take your beginning and ending bank balance for each of the last three months, average them, and apply the formula. That number, annualized, is money your bank isn’t earning you, because your bank never told you the tradeoff was optional.

FX Markups: The Spread That Doesn’t Appear on Any Statement

If you’re paying international contractors, vendors, or suppliers, or receiving payments from foreign customers, your bank is probably taking 2–3% of every transaction. Not as a fee line item, but as an embedded spread between the rate you get and the mid-market rate at the time of the transaction.

Say you’re moving $50,000 per quarter to international vendors. At a 2.5% embedded spread, you lose $1,250 per transaction, or $5,000 per year, to a markup that doesn’t appear anywhere on your bank statement. The Wise report found $24.4 billion in undisclosed FX fees hit small businesses in 2024.

You can audit this yourself. Pull your last three months of international payments. For each transaction, find the mid-market rate at that date using xe.com’s historical rate tool. Calculate the percentage difference between the rate you received and the mid-market rate. That percentage is your effective markup. Apply it to your quarterly payment volume and annualize.

Most founders who run this exercise are surprised. The average markup sits at 2–3%, but some banks push 4–5% on less common currency pairs. For a startup doing regular international payments, this is a real budget line that doesn’t exist anywhere in your financial reporting, which is exactly the point.

Manual Financial Admin: The Cost That Never Shows Up on a Statement

AP/AR workflows running through a bank with no automation integration generate a specific kind of cost: time that could be spent building, selling, or hiring, spent instead on pulling invoice PDFs, matching transactions, exporting to accounting software, and chasing overdue payments.

The numbers add up faster than most teams expect. Finance teams handling invoice processing routinely spend 10 hours per week on these tasks. At a $120 per hour blended cost (a reasonable benchmark for an operations manager or senior employee at a growth-stage startup), that’s $62,400 per year in direct opportunity cost.

Fragmentation compounds the hours. When your banking data lives in one system, invoices sit in another, and reconciliation happens manually in a third, you pay for the errors, the duplicates, and the audit gaps that appear when data crosses those seams. Every custom script built to export bank data, auto-fill invoice templates, or sync payments to your accounting system is maintenance debt with a zero-line-item cost that accrues every quarter.

Why You Haven’t Switched, and Why the Reasoning Doesn’t Hold

The three objections that come up most often are KYC friction, integration risk, and timing.

- KYC friction: The mental model most founders carry comes from the last time they opened a business bank account — paperwork, in-person verification, a week of waiting. Digital-first fintech platforms now handle EIN submission, business documentation, and Plaid-based identity verification entirely online, covering LLCs, C-Corps, and S-Corps, with no branch visit and no mailed forms required.

- Integration risk: The fear is valid but overstated. If you’ve built your accounting workflow around QuickBooks or Xero, moving your banking layer doesn’t have to touch that at all. Platforms that integrate directly with both tools will auto-sync T-bill gains and losses and paid invoices without requiring any manual reconfiguration. Your accounting workflow stays exactly as it is.

- Timing: This one is largely self-created. You don’t have to migrate your full payments infrastructure on day one. If you have /$500K sitting in a checking account earning nothing, you can move that idle cash into a yield-bearing product today while your existing operating account stays put. Payments infrastructure migrates on your schedule.

Switching cost is a one-time event. Banking inertia at $4,400–$7,200 per year is a perpetual subscription you never agreed to pay.

What Agent-Native Banking Changes About Each Line Item

Meow is the only business banking platform that addresses all four of these cost vectors in one place. The direct mapping:

Treasury. From the Meow Treasury Dashboard, you set up a T-bill ladder by selecting your maturity preference (4-week, 8-week, or 13-week) and enabling auto-roll. When a T-bill matures, the platform automatically reinvests the proceeds into a new T-bill of the same duration, or routes funds back to your checking account if you’ve configured it that way. If you need liquidity before maturity, you can sell on the secondary market same-day directly from the dashboard, with no trading fees. The fee structure is 1 basis point per month (annualized), with no trading fees and no hidden spreads. Meow’s direct competitors don’t publish their treasury fee structure with that level of specificity, which makes comparison difficult by design.

T-bill gains and losses auto-sync to QuickBooks and Xero, removing the manual export step entirely.

FX. Meow manages foreign currency payments across 50+ currencies via its Airwallex partnership, with up to 2% savings compared to traditional bank spreads. For companies accepting or holding crypto, Meow also supports stablecoin payments and free USDC on/off-ramping via BVNK. Both sit in the same dashboard where you’re managing your T-bill ladder.

Agentic AP/AR. Meow ships a live MCP server at https://mcp.meow.com/cli and a CLI you install with:

1npm install -g @joinmeow/cliFrom the MCP interface, AI agents (Claude, ChatGPT, or any OpenAI-compatible agent loop) can check balances, review transactions, manage invoices and bills, look up contacts, issue virtual cards, and draft payments, all operating with scoped API keys that define exactly what each agent can do. One agent reviews incoming bills; a separate agent handles outbound invoices. Each has independent permissions.

Payments initiated through the MCP server are always recorded as drafts in a pending-approval state until a human confirms, so the control layer is built into the workflow.

Migration. QuickBooks and Xero integrations cover the accounting side automatically. Paid invoices update your books, and your accounting workflow stays unchanged when you add Meow’s treasury or payments layer. There’s nothing in your existing setup to break.

Run the Audit: Four Steps You Can Complete This Week

The practical path from suspicion to a real number runs four steps.

- Pull 90 days of bank statements. Flag every line item: monthly maintenance, wire fees, ACH fees, service charges. Sum them and multiply by four to annualize. This is your fee baseline, the costs that actually appear on paper.

- Calculate your average monthly idle balance: (beginning balance + ending balance) ÷ 2. Multiply by the current 4-week T-bill rate minus your checking APY. Annualize. If you’re holding $400K and earning 0%, a 4.3% T-bill rate means you’re leaving $17,200 per year on the table.

- Pull all international payments from the last 90 days. For each, find the mid-market rate at that transaction date via xe.com’s historical rate tool. Calculate the percentage difference from your executed rate. Apply that markup to your quarterly international payment volume and annualize.

- Time one complete AP/AR cycle from invoice receipt to payment and reconciliation. Multiply by your annual number of pay cycles, then multiply by your blended hourly cost. This is your labor exposure: the number that compounds every time you add a vendor or hire someone to manage the backlog.

Add the four numbers. That total is your annual banking inertia cost.

If the number is meaningful (and for most growth-stage startups it will be), the next step is straightforward: open a Meow account at meow.com, move idle cash into a T-bill ladder from the Treasury Dashboard, and connect Meow’s MCP server to your agent stack for the next AP cycle. The audit and the fix can run in parallel.

Final Thoughts

Founders who act on this analysis switch banks because they ran the numbers. Inertia at $4,400–$7,200 per year, before accounting for yield deltas on idle balances, FX on international payment volume, or engineering hours spent maintaining financial data pipelines, stops being a reasonable tradeoff once you can see it clearly.

You already have the inputs. The calculation takes an afternoon. Start at meow.com.

Frequently Asked Questions

What is the yield gap in business banking, and how do I calculate it?

The yield gap is the difference between what your checking account pays and what short-duration Treasuries or money market instruments currently yield. To calculate it: subtract your checking APY from the current T-bill rate, then multiply by your average idle cash balance. Average your beginning and ending bank balance over the past three months to get that idle balance figure.

Are business checking accounts at fintech platforms FDIC insured?

Most fintech banking platforms hold customer funds at FDIC-insured partner banks rather than holding a bank charter directly. This means coverage applies, but the $250,000 limit applies per depositor per bank. If you consolidate balances above $250,000 at a single fintech platform, verify how many underlying partner banks are used and whether pass-through coverage applies to your account type.

How do banks hide FX markups on international payments?

Banks apply FX markups as a spread between the mid-market exchange rate and the rate they offer customers, not as a separate fee line item. At a 2.5% markup on a /$50,000 international payment, /$1,250 disappears in the transaction with no statement entry. To audit this, pull your last 90 days of international payments, look up mid-market rates at those dates on xe.com, and calculate the percentage difference from your executed rate.

How much engineering time does a typical bank integration consume?

A single bank integration typically requires 2–4 weeks of initial engineering time and 1–2 weeks per year of ongoing maintenance. API changes at the bank level, which happen without consistent notice, can trigger unplanned rewrites. Across multiple banking relationships, this accumulates into a meaningful fraction of an engineer’s annual capacity.

What is a T-bill ladder and how does it work for business treasury management?

A T-bill ladder is a strategy where you purchase Treasury bills with staggered maturity dates so that cash becomes available at regular intervals. As each bill matures, proceeds are either reinvested into a new T-bill of the same duration or returned to your operating account. This provides predictable liquidity while keeping idle cash in a yield-bearing instrument rather than a low-interest checking account.

What is an MCP server in the context of business banking?

An MCP (Model Context Protocol) server is an interface that allows AI agents, such as Claude, ChatGPT, or any OpenAI-compatible agent, to interact with external services using structured, permissioned API calls. In the context of Meow’s banking platform, the MCP server lets AI agents check balances, manage invoices, issue virtual cards, and draft payments, each with scoped API keys that limit what any individual agent can access or execute.

How do I switch business banks without disrupting my accounting workflow?

The lowest-friction migration path is to add a new banking layer for idle cash first while keeping your existing operating account in place. Platforms that integrate directly with QuickBooks or Xero will auto-sync transactions without requiring you to reconfigure your existing accounting workflows. Full payments infrastructure migration can happen on your own schedule after the yield layer is running.